Cash Out Day 2026 is more than a grassroots protest — it is a defining moment for financial inclusion, multicultural equity, and the right of every Australian to participate in the economy on their own terms.

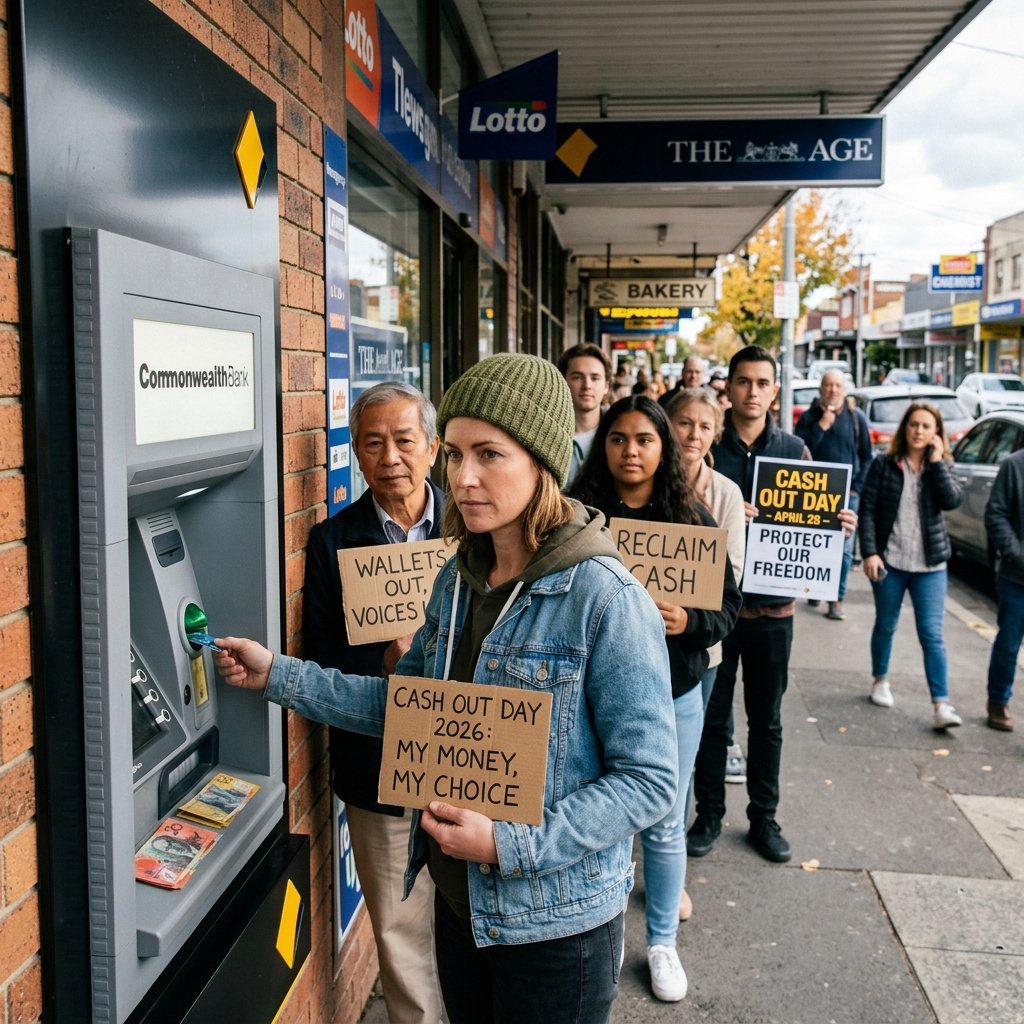

Today, across suburbs, shopping strips, and regional towns from Broome to Brunswick, Australians are joining a quiet but powerful act of financial resistance. They are walking up to ATMs, inserting their cards, and withdrawing cash — not because they have to, but because they believe they should always have the choice.

This is Cash Out Day 2026. And while it may look like a simple bank transaction from the outside, for millions of Australians — including migrants, elderly residents, people with disabilities, and communities in outer regional areas — it represents something far deeper: the right to be included in an economy that is rapidly leaving them behind.

What Is Cash Out Day?

Cash Out Day is an annual, community-led campaign encouraging Australians to withdraw physical cash from ATMs and bank branches as a visible statement against the accelerating move toward a cashless society. This year’s event falls on Tuesday, 28 April, and is championed by Jason Bryce, founder of advocacy group Cash Welcome.

According to a report published by 7NEWS, Bryce hopes as many as two million Australians will participate today, filling their wallets as a collective signal to banks and policymakers that cash is not a relic — it is a right.

“I think Aussies need to show the PM and the banks that cash is important to all of us as a reliable, private, surcharge-free payment option,” Bryce told 7NEWS.com.au ahead of today’s event.

The campaign has grown significantly since its predecessor, “Draw Out Some Cash Day,” held on 2 April 2024, which drew long queues outside bank branches and sparked national conversations about financial freedom. The message has not changed. But the urgency behind it has sharpened.

The Shrinking Infrastructure of Cash

To understand why Cash Out Day matters, you need to understand what has already been lost.

Australia once had nearly 14,000 bank-owned ATMs in 2017. By mid-2023, that number had been slashed to approximately 5,700 — less than half — according to data cited by 7NEWS and financial research agency Canstar. Since then, a further 217 ATMs have been removed. In the last financial year alone, almost 450 branches and ATMs were closed nationally.

The figures are even more striking in regional Australia. A January 2025 Reserve Bank of Australia (RBA) bulletin on Access to Cash in Australia revealed that while 95 per cent of people in major cities live within 1.6 kilometres of a cash withdrawal point, those in outer regional areas face average distances of 16 kilometres, with remote Australians travelling up to 32 kilometres, and those in very remote communities averaging 95 kilometres to the nearest withdrawal point.

For anyone living outside a capital city, “just use the ATM” is not a simple suggestion. It can be a half-day journey.

Who Bears the Burden? The Human Cost of Going Cashless

Here is where the numbers become faces.

Across Australia, approximately 1.5 million people rely on cash for the majority of their everyday in-person transactions, according to analysis published by the RBA. Among them are some of the country’s most vulnerable residents — elderly Australians, people with disabilities, and members of culturally and linguistically diverse (CALD) communities who may have limited digital literacy or limited access to mainstream banking services.

Consider what this means for a grandmother in Footscray who does not own a smartphone. Or a newly arrived humanitarian entrant in Logan who does not yet have a credit history to open a digital banking account. Or an elderly Vietnamese-Australian man in Cabramatta who has trusted cash his entire adult life and finds digital payment interfaces confusing and alienating. For these Australians, the disappearance of cash is not an inconvenience — it is exclusion.

Research cited by uutyler.org estimates that approximately 1.3 million Australians over the age of 65 and 1.1 million people with disabilities face significant digital exclusion — meaning they lack consistent access to, or capability with, the digital tools that an increasingly cashless economy assumes everyone possesses.

The pace of ATM and branch closures has deepened these vulnerabilities. Western Australia alone lost 339 bank branches — nine per cent of its total — in a single year, according to Canstar’s analysis. Victoria, home to some of the country’s most diverse multicultural communities, now has just 1,500 ATMs statewide.

“The banks are trying to force everybody online, even if it means taking away people’s independence,” Melbourne disability advocate Heather Lewis told journalists last year. “It’s not right and it’s not fair. It should be my choice if I want to use cash.”

Her words carry weight that extends far beyond her own experience.

The Government’s Response: A Mandate, But With Gaps

To its credit, the Australian Government has acknowledged the problem. Treasurer Jim Chalmers announced that from 1 January 2026, major fuel and grocery retailers would be legally required to accept cash for in-person transactions of up to $500, between 7am and 9pm. According to reporting by tanea.com.au and confirmed by The Adviser, the mandate is designed to ensure that essential services remain accessible to cash-dependent Australians.

On the surface, this is a meaningful step. In practice, campaigners argue the mandate is too narrow to carry real weight.

Bryce has publicly described it as “the world’s weakest cash mandate,” noting that it exempts small businesses with an annual turnover under $10 million — which includes the corner stores, local cafes, and neighbourhood pharmacies that many multicultural community members rely on daily. The mandate also does not address the systemic collapse of ATM infrastructure, which is the very mechanism through which people access cash in the first place.

The Reserve Bank has backed cash acceptance as a matter of financial equity, and a Treasury consultation is underway examining the sustainability of Australia’s broader cash distribution network. Industry data shows that Armaguard, which distributes the majority of Australia’s physical currency, has warned that its operations are becoming increasingly unviable as demand falls — raising the prospect of a cash distribution crisis that could hit regional and remote communities hardest.

Why This Matters to Multicultural Australia

For The Australian Canvas, this story is not simply about notes and coins. It is about who gets to participate fully in Australian economic life — and who gets quietly left out.

Australia is one of the most culturally diverse nations on earth. According to the Australian Bureau of Statistics, more than half of Australians were either born overseas or have at least one parent born overseas. Within that diversity are communities — particularly from Southeast Asia, South Asia, the Pacific Islands, the Middle East, and Africa — where cash economies have historically been the norm, where distrust of digital financial systems runs deep, and where elders within those communities may have spent decades building trust in physical money as the cornerstone of their financial independence.

A cashless future built without these communities in mind is not progress. It is exclusion dressed up as convenience.

This is also a First Nations issue. Many remote and very remote Aboriginal and Torres Strait Islander communities face some of the most acute challenges around cash access, with ATM distances of up to 95 kilometres confirmed by RBA data. Financial autonomy, privacy, and freedom from surveillance are not abstract principles in these communities — they are lived necessities.

What Comes Next

Cash Out Day 2026 will not reverse the trajectory of digital payments. That was never the point. What it can do — and what it is doing today — is keep the conversation alive long enough for policy to catch up with people.

The community-led push for stronger cash mandates, regulated ATM infrastructure standards, and culturally inclusive financial services is growing. And it deserves support not just from advocates, but from politicians, regulators, and the banking sector itself.

Because a society’s values are reflected not only in who it celebrates, but in who it chooses not to leave behind.

Today, as millions of Australians stand at ATMs across this country, they are not just withdrawing money. They are making a deposit — into the idea that an inclusive economy is not optional. It is essential.